The Credit Process:

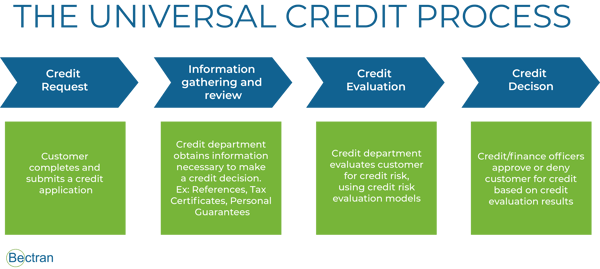

At a high-level, any credit transaction involves four key process areas, which we call the Universal Credit Process (UCP):

As shown above, this process involves a set of sequential tasks that are often time-consuming and, in some cases, complex and financially risky.

As of today, many businesses still operate on a traditional task execution model. This could mean applications are sent out as paper or PDF documents, key tasks such as information gathering are executed manually and risk assessment is based on rule of thumb or spreadsheet computations.

The traditional credit process is manually intensive, slow and prone to errors.

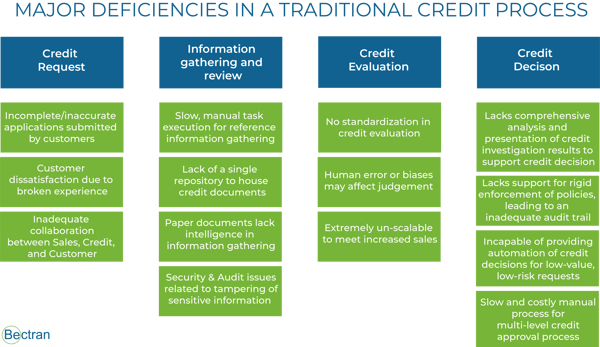

PROCESS DEFICIENCIES

Listed below are major deficiencies that are prevalent in the traditional credit process, broken down by the UCP:

These deficiencies often lead to an increased timeframe in approving and setting up new customers for credit, and create other costs and risks for the business. Most importantly, these deficiencies slow down the Sales Process, and in some cases, jeopardize sales and hurt customer satisfaction.

COSTS AND RISK TO BUSINESSES

These shortfalls bring various disadvantages to any business, along these lines:

As shown in the illustration above, the costs and risks associated with a traditional credit process can range from customer dissatisfaction to security breaches. In order to operate effectively, businesses must be able to ensure their costs and risks are kept in a highly secured transaction processing environment. To achieve these goals, many businesses are turning to technology solutions.

TECHNOLOGY SOLUTION

The question now is --- how can technology help expedite these key process areas? Bectran has identified certain key areas where technology can help a company avoid these deficiencies and ultimately shorten its credit-to-cash cycle.

- Accuracy/Completeness: An electronic application system can reduce numerous hours spent obtaining complete and accurate information by enforcing required fields and smart document uploads.

- Security/Audit: A secure and robust credit management system ensures that confidential information is handled in the right manner and is visible to only the authorized personnel. It also provides a clear audit trail of all information entry and decisions, as well as any other actions on an application.

- Visibility: Systems to track and report the progress of a credit application can help reduce unnecessary communication between the Customer, Sales Department and the Credit Department, as well as provide the customer with real-time updates.

- Information Gathering Automation: One of the biggest advantages of a smart credit management system is its ability to automate various information gathering tasks. Such a system could automatically gather key pieces of information, such as:

- References (bank/trade)

- Tax certificates on expiry

- Credit reports based on information from the application

- 5. Robust Credit Risk Assessment: It is imperative that a thorough risk analysis is performed in order to reduce bad debt and potential collection costs. A credit management system can incorporate varying pieces of information along with the ability to customize attributes and weights to mirror various evaluation criteria.

- 6. Clear approval workflows: Smart credit management systems can provide businesses with clear workflows for approval, which help ensure that all key processes are followed and nothing slips through the cracks.

- 7. Speed: Instant Credit Decisions can be achieved with a system that is able to analyze and approve a credit application based on pre-configured criteria and decision rules. This would ensure that customers are set up in seconds, thereby reducing a company’s order-to-cash cycle.

- 8. Flexibility: A flexible credit management system ensures that changes can be implemented as needed and on an ongoing basis, giving the company the power to direct change.

Bectran has helped companies across multiple industries to make the transition to cost-effective, comprehensive technology solutions with the benefits listed above.

For more information or to request a free online demo, reach out to sales@bectran.com.

About Bectran [www.bectran.com]

Bectran, the industry leading SaaS platform, has grown rapidly over the years to become the companion toolkit for the credit department just as CRM is for the sales department. From simple to complex organizations and SMEs to Fortune 500 companies, Bectran has helped companies cut down the time to process and approve credit by over 90% whilst significantly lowering the risk of credit defaults and the cost of collections.

A growing number of companies are depending on Bectran to manage their Accounts Receivable and Collections. With significant process and task automation, companies can cut down the cost of collections by as much as 60-90% while accelerating the cash receipts cycle with complete and accurate cash applications.

Bectran’s clients enjoy the ease, speed, and cost-effectiveness of adopting the Bectran platform. New clients are on-boarded in a matter of days or weeks. Credit professionals in various industries have described the Bectran platform as the future of the credit department.

Ali Kidwai is a Platform Services Specialist at Bectran. He is focused on helping customers implement the best solution strategy on the Bectran platform. View posts by Ali Kidwai.

Ali Kidwai is a Platform Services Specialist at Bectran. He is focused on helping customers implement the best solution strategy on the Bectran platform. View posts by Ali Kidwai.

The views expressed on this blog are those of the author and do not necessarily reflect the views of Bectran. This blog may contain links to content on third-party sites. By providing such links, Bectran does not adopt, guarantee, approve, or endorse the information, views, or products available on such sites.

Interested in writing for Bectran Blog? Send us a pitch!

-1.png)

.png)

-1.png)